Weekly Coal Index Report

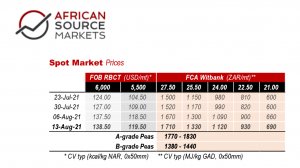

If South African coal exporters are buzzing with excitement at spot prices of around $140/t, they are surely eyeing their Australian counterparts with sweaty palms.

At just over $170/t, Newcastle is near its record highs, whilst Indonesian coal, favoured by China after its Australian ban, has breached its all-time highs already.

As climate negotiators gear up for COP26 and Asia acquiesces on the verbal front, when it comes to action, they are building ever greater coal- and liquefied natural gas-fired capacity. The world simply cannot get enough electrical power, especially as electric vehicles enter the mainstream.

European power and natural gas prices have come off their recent boil of late, while crude continues in a bearish drift south.

In South Africa, Transnet has kyboshed all hope of Botswana coal exports, as it confirms there are no plans for a South African border corridor line, and no plans to extend the Waterberg line beyond six-million tonnes a year.

Further, Transnet Freight Rail does not plan to extend the Richards Bay Coal Terminal (RBCT) line capacity beyond 81-million tonnes a year, believing that export coal demand will have dropped significantly by the mid-30s.

Meanwhile, local rail performance remains beset with issues and RBCT itself suffered a power outage last week, briefly halting vessel loading.

Unless China can be reigned in, plans by Blackrock et al. to purchase coal-fired stations and shut them down early is likely only a drop in the proverbial ocean. Mycelium must be daunted by all that carbon needing to be turned into new coal seams.

Technicals suggest that we are, once more, quite far into overbought territory, although not as overbought as we were in January. This is the nature of momentum analysis, and it would suggest that there is perhaps a little more upside left.

However, the bulls must surely be quite exhausted by now, and looking forward to a little rest and relaxation after a hot and heavy summer run. Although with the weekly signal line indicating that trend is still firmly in positive terrain, the bears are going to have to remain in hibernation for some time.

No doubt they will get their time at the wheel, but 2021 is just not the year for the bears.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

Sika South Africa is a trusted partner for the nation’s infrastructure, commercial, residential, and industrial sectors.

VISIT SHOWROOM

ECG provides specialised electrical engineering services to the Mining, Utilities, Materials Handling and Industrial industries, with extensive and...

VISIT SHOWROOM

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation