Weekly Coal Index Report

Although coal prices are a little off their highs, talk is already abounding of new coal mine investment… everywhere except for South Africa it would seem.

Botswana and Tanzania are turning to Chinese investors to develop new coal reserves and rail link lines. In the case of Tanzania, a major new bulk export port is also planned.

Botswana coal is probably the most viable option to plug a major coal supply cliff from 2030, but it depends on getting Transnet Freight Rail (TFR) to integrate an export rail line into its South African coal corridor.

Meanwhile, TFR is still struggling to deal with rail reliability amidst rampant theft and maintenance issues. The lack of rail and tightness of coal supplies could see annualised Richards Bay Coal Terminal tonnages at only the same level as last year, which would be a shame amidst such high prices.

Although coal supply remains subdued in China, domestic prices are expected to cool as production resumes from previously suspended capacity, with larger quotas for mines now approved as well.

As European gas, power and oil markets all experience choppy prices, one trend seems to be emerging… with wilder weather caused by climate change, utilities will most likely come to rely more and more on reliable baseload fuels such as coal and gas, that can be stored and burned at will. Carbon prices are not sufficiently onerous enough to prevent ongoing gas-to-coal switching.

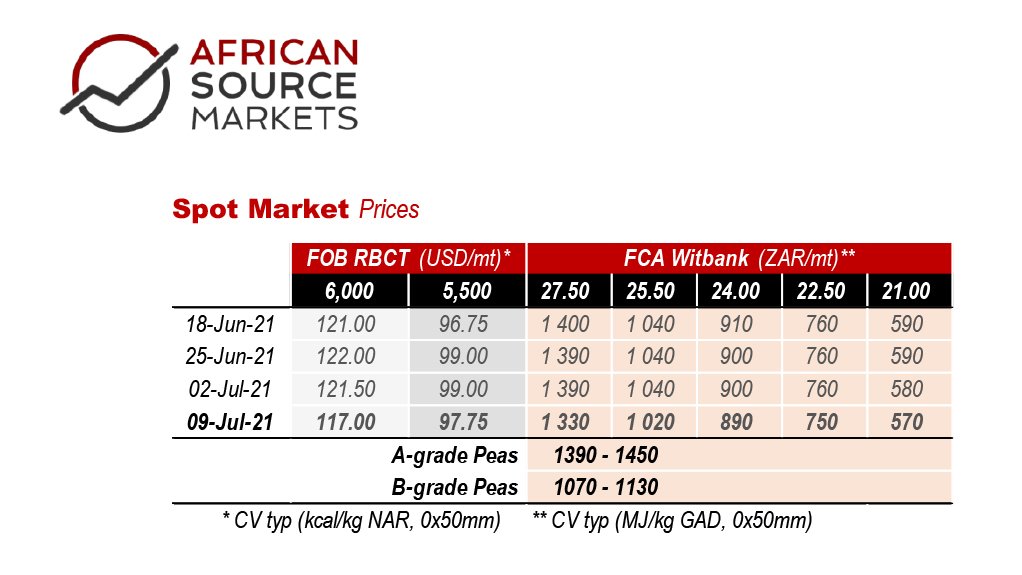

Short term momentum (MACD) continues to fall, taking some pressure off overheated prices. However, with medium term trend remaining strongly positive, it’s unlikely that these early price falls will precipitate any major drop in price.

Hence, we would expect RB1 to linger around the $120 mark for a little while yet. Physical constraints on supply should see RB1 start to close the gap with Newcastle in due course, and momentum is clearly giving us a breather to enable price to rise once more in a few weeks time.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

Virtual Gas Network supplies compressed natural gas via a virtual gas distribution network.

VISIT SHOWROOM

Your global lifecycle technology & service partner for materials & minerals processing equipment for coal, iron ore, copper, manganese & other...

VISIT SHOWROOM

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation