Weekly Coal Index report

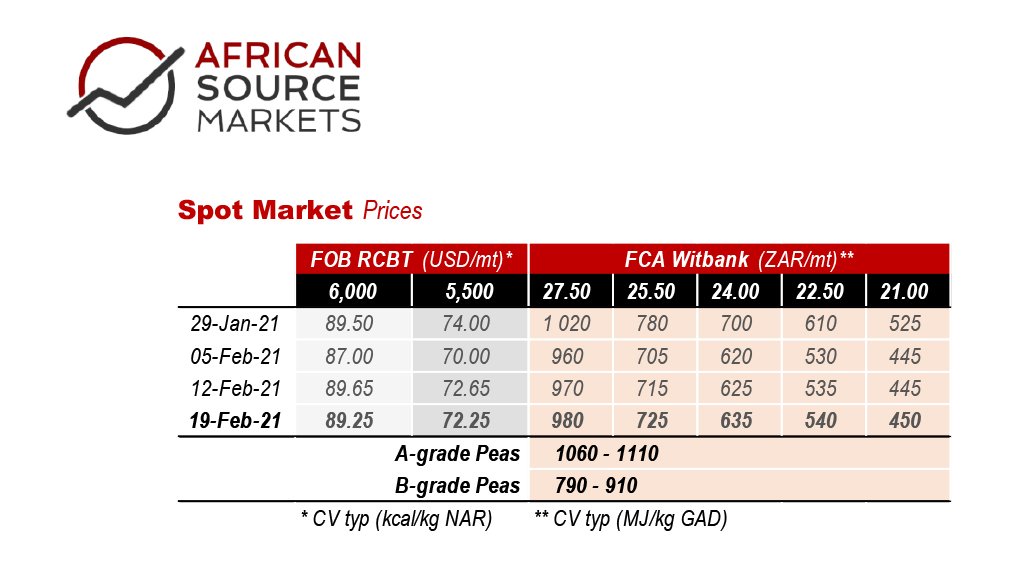

European power and gas prices had a volatile week as recent cold weather subsided. However, coal prices held up well, in a sign that strained renewable power grids tend to fall back on coal and gas as solar power fades, and wind turbine blades ice up. With frozen seas impacting on Russian coal supplies, and sharply higher European coal demand, panamax rates have seen a surge to multi- year highs in the Atlantic.

India has once again proposed new rules to liberalise the sale of domestic coal from captive, State-owned mines, in a move to try and reduce the country’s reliance on imports. As one of the world’s largest coal producers, Coal India could do real damage to South African exporters if it gets its act together to liberalise its coal sector.

Chinese domestic coal prices stabilised from recent weakness, as demand pick ups after the new year holiday. South Africa appears to be dithering over any concrete future energy plans.

As the rest of the world commits to full decarbonisation by 2030 to 2050, South Africa appears to mostly be asleep, with much talk of liquefied natural gas, hydrogen, nuclear and renewable plans, but little action to support investment. The longer this situation continues, with no major replacement plans for coal plants, the worse the pain is going to be by 2030, as Eskom stares down the barrel of having to keep aging coal plants open, with domestic coal prices enjoying new highs.

Spot prices remain firm, although the back of the curve is weaker as risk is rolled into the future. Momentum continues to subside, setting up nicely bullish conditions for coal producers going forward. This time last year both price and momentum had rapidly collapsed from the fourth quarter of 2019 squeeze, whilst this year conditions have conspired to keep prices firm.

Of course momentum still has a long way to go to reach an oversold level, and the forward curve suggests the loss of several dollars over the next couple of months. However, if one had to hazard a guess for the next floor level, it would be around $70 by July before we perhaps see further cyclical strengthening.

Like all commodities, coal prices are of course also benefitting from a structurally weaker Dollar, even though inflation is not really in sight yet. This trend is an interesting one to watch as confidence in the dollar continues to erode. The US treasury market is now also a key factor to watch in the evolution of most commodity prices going forward.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

Virtual Gas Network supplies compressed natural gas via a virtual gas distribution network.

VISIT SHOWROOM

Your global lifecycle technology & service partner for materials & minerals processing equipment for coal, iron ore, copper, manganese & other...

VISIT SHOWROOM

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation