Weekly Coal Index Report

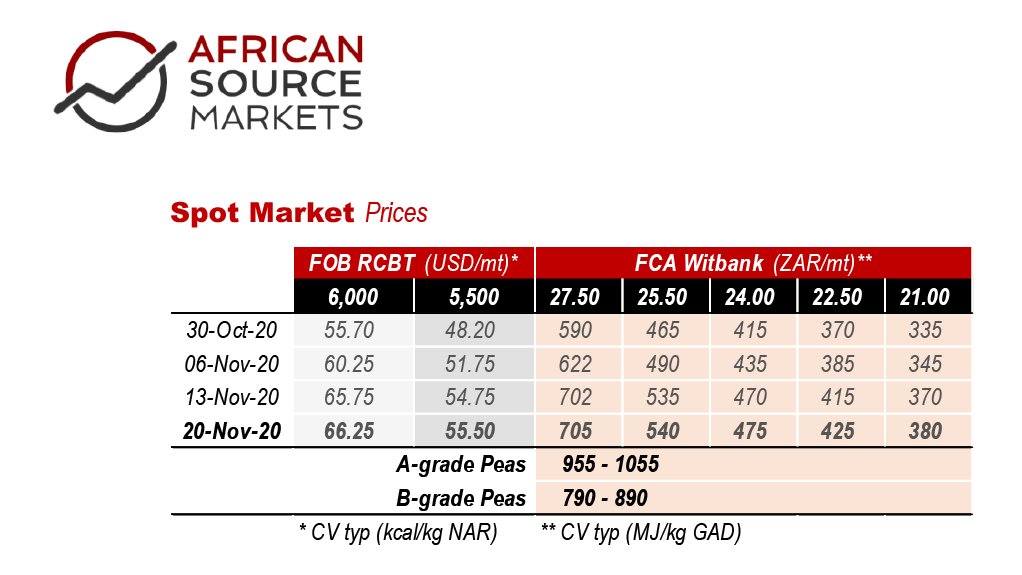

Coal markets had a volatile week, as Chinese import restrictions may be lifted, whilst severe weather is affecting Newcastle port loadings. RB1 prices rallied slightly although the ZAR continues to strengthen, despite further sovereign credit downgrades by Moody’s.

Chinese officials are considering starting to restrict the further development of coal-fired power plants from the 14th five-year plan for 2021-2025. With half of China’s coal capacity less than 10 years old, and around 100 large plants already under construction, there is no need for more if the country wants to avoid stranded assets under Xi Jinping’s carbon neutrality plans by 2060.

Meanwhile, Japan is enjoying lower coal demand amidst increasing nuclear plant availability, although a cold winter could see a higher than expected coal burn. The latest insurance and investor group calling for an end to coal is the United Nations-convened “Net-Zero Asset Owner Alliance”, representing over $5-trn in assets under management. Their research shows that by 2030, around half of global thermal coal capacity will be loss-making.

In South Africa, as Eskom mulls the closure of several of its RTS stations, the lastest G20 report on Climate Transparency indicates that SA needs to reduce emissions to below 348 Mt CO2e by 2030 and to below 224 Mt CO2e by 2050 to be within a 1.5°C Paris-aligned “fair-share” pathway.

Short term trend momentum (MACD) is running nicely towards its previous peaks around the 4-5 level now. It should reach this within the next 2 to 3 weeks, at which point the market could be considered “overbought”.

However, price action is lacking in vitality and we are nowhere near the previous price peaks of last year. Perhaps we will not peak this year and a less volatile market will emerge in 2021, with more of a sideways drift in price, as momentum slowly erodes back down again?

Either way we should continue to see sustained price pressure to the upside for now, although short term corrections are possible to slow the upwards move.

Early next year may prove to be a fortuitous time for miners to lock into forward price sales, considering that the forward curve is flat to slight contango for 2-3 years

out.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

CMTS is a leading, well-established EC&I contractor with 37+ years of mining and industrial experience. We execute full-scope EC&I projects with...

VISIT SHOWROOM

ZF Aftermarket is the after-sales division of the world-renowned German ZF group, a global leader in mobility technology.

VISIT SHOWROOM

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation