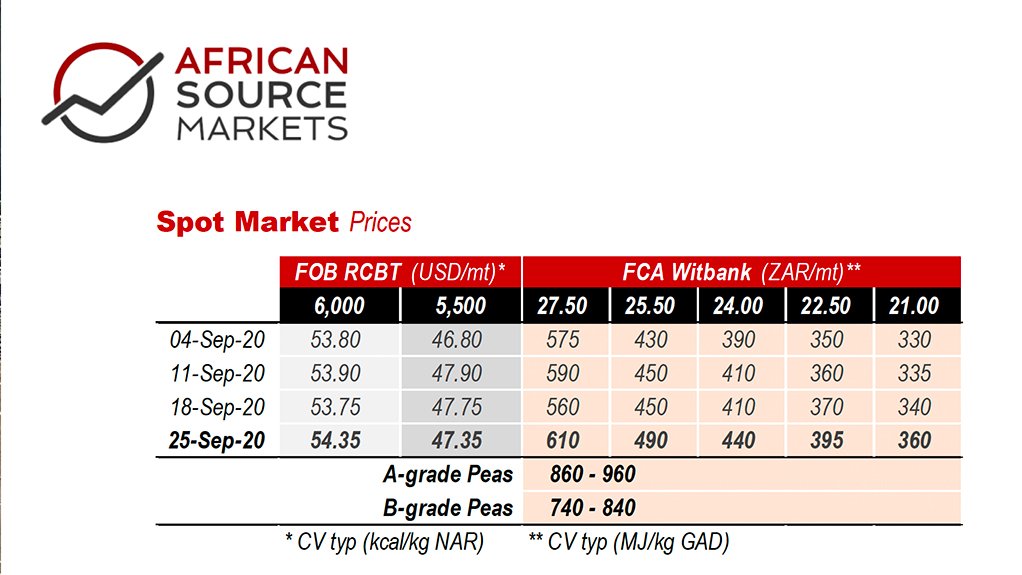

Weekly Coal Index Report

As mining firms around the world cut back supply, Glencore has announced even further production cuts at its Australian operations. These cuts, alongside nuclear outages caused by typhoon activity, have helped South Korean import coal prices remain firm. However, the imminent return of nuclear capacity may soon alter coal’s fortunes.

Chinese domestic prices are also firm, with several Chinese ports seeking to ease their import restrictions in order to clear their existing coal stocks at the ports. Meanwhile, Coal India remains bullish on coal demand going forward, even as renewables gain support in the country. Over 16 new mining projects have been authorised by Coal India this year, potentially adding some 120 Mtpa of domestic production.

Freight prices enjoyed a bullish week, with capesize rates up significantly, notably on fronthaul fixings. Higher freight is generally bearish for RBCT coal into India etc., although API#4 gained on the week as well, as European power and emissions gained support, alongside stable gas prices.

President Cyril Ramaphosa dedicated his weekly newsletter to the energy crisis in South Africa, in a move by cabinet appearing to endorse renewables. Eskom is juggling several balls, including a Just Transition away from coal, alongside several operational, emissions and financial problems.

The coal market is adrift in a sea of uncertainty. Volatility is lifeless as the Bollinger Bands close in to the tightest they have been in a long time, albeit opening some room on the downside now.

Short-term momentum (MACD) appears to have stalled from its recent march upwards, although it remains in slightly positive territory. The signal line is sloping up but still ever so slightly in negative territory. It really needs to push up some more for the bulls to shift into the driver’s seat.

The concern of course is that momentum must at some point inevitably fall once more. This aimless drift upwards could thus be broken anytime now by a sudden sharp downside move that could flush out all but the strongest of longs.

With the rest of the energy complex and global markets trying to stage a recovery, there is still some wiggle room for the bulls to try push higher - for now…

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

North Ridge Pumps is an independent manufacturer of pumps. We have a proven track record for product support and customer service throughout the...

VISIT SHOWROOM

Rittal is a world leading provider of top-quality integrated systems for enclosures, power distribution, climate control, IT infrastructure and...

VISIT SHOWROOM

Press Office

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation