Metals make climate change mitigation possible – Citi Research

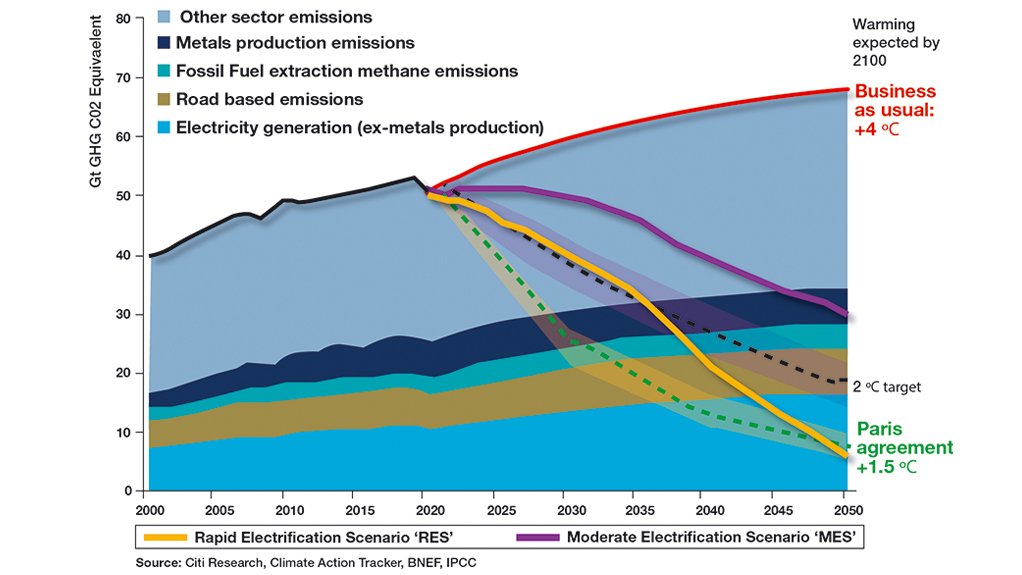

JOHANNESBURG (miningweekly.com) – In a rapid electrification scenario, metals have the ability to bring about the reduction of close to 1 000 gigatonnes (Gt) of global greenhouse gas (GHG) emissions by 2050, Citi Research states in a note that examines the metals industry’s potential contribution to climate change mitigation over the next 30 years.

Examined is the potential of the metals industry itself to develop methods to evaluate the relative climate impacts of 16 metals across the complex – steel, aluminium, copper, nickel, zinc, lead, gold, silver, platinum, palladium, rhodium, lithium, cobalt, ferrochrome, vanadium and rare earths.

This is the first of a Citi series aimed at evaluating the metals industry as well as individual metals in the context of the Sustainable Development Goals (SDGs) of the United Nations (UN), beginning with UN SDG 13 on climate change, since it is widely thought to be one of the most important challenges for humanity.

Citi’s finding is that the metals industry is critical to facilitating the bulk of the decarbonisation that the Paris Agreement requires by 2050.

The metals industry is able to do this by enabling the shift to:

- renewable energy;

- the electrification of transport;

- the development of carbon capture and storage (CCS); and

- through the reduction of emissions from metals production.

Cumulative global GHG emissions in Citi’s rapid electrification scenario are well above the carbon budgets of 420 Gt to 580 Gt for the 1.5o Intergovernmental Panel on Climate Change scenario.

In order to meet the Paris agreement:

- CCS will need to do more; and

- other sectors such as agriculture, waste, and industrial processes will have to do their fair share, which is an assumed nil contribution.

The note, compiled by eight analysts, states that all emissions directly and indirectly related to the metals industry, including the 16-plus metals markets, could well be deeply emissions negative over the vast bulk of the period through 2050, in both their moderate and rapid electrification scenarios.

Most notably green hydrogen in steelmaking has the potential, the note states, to reduce scope 1, 2 and 3 emissions from the metals sectors even further than the analysts’ rapid electrification scenario calculates. The recycling of metals, and in particular battery metals, is cited as a further means by which the carbon intensity of metals production can be lowered.

Moreover, the ‘second life’ of certain products, such as the repurposing of electric vehicles into energy storage, adds another perspective by which metals' ‘net’ emissions reduction can be calculated to be higher through their lifecycle.

Because steel volumes account for the vast bulk of metals production growth in both the moderate and rapid electrification scenarios, steel's value weight is the highest by some distance, despite its lower value per tonne compared to many other metals. This leaves steel the biggest contributor to the net reduction in emissions. Critically, all metals in the rapid electrification scenario are substantial net contributors to climate change mitigation over the period, with copper second and aluminium third to steel.

Substantial investment and contributions to decarbonisation are required across all emitting sectors. At present, electricity generation accounts for about 13 Gt of global GHG emissions, or 25% of total, though it is 11 Gt or 21% of total, excluding the metals sector.

Road transportation accounts for 7 Gt, which is 13% of total. The agricultural sector accounts for 6 Gt, which is 11% of total. Metals production accounts for 5 Gt, which is 10% of total including grid-based emissions. Cement production accounts for 4 Gt, which is 8% of total excluding the grid. Fossil fuel extraction accounts for 4 Gt (7% of total), buildings for 3 Gt (6% of total) and nonroad based transportation for about 2 Gt (4% of total).

Looking ahead, the analysts’ forecasts in the moderate electrification scenario are for metals sector emissions to grow only slightly from about 5.1 Gt a year in 2019 to about 5.5 Gt by 2050 and in the rapid electrification scenario to fall to about 3.5 Gt a year, owing to expected reductions in the emissions intensity of metals production.

To decarbonise the world, the note states that a portfolio of mitigation needs to be developed and implemented across the highest carbon-emitting sectors. It is calculated that although the pace of innovation has accelerated and investment has increased, the investment gap between what is being spent and what needs to be spent is a high $3-trillion a year to more than $5-trillion a year.

Comments

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

Our Easy Access Chute concept was developed to reduce the risks related to liner maintenance. Currently, replacing wear liners require that...

VISIT SHOWROOM

Education: Consulting with member companies to obtain the optimal benefits from their B-BBEE spending, skills resources as well as B-BBEE points

VISIT SHOWROOM

Press Office

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation