US mining industry in flux as policy, economic and enviro challenges force change

DWINDLING DEMAND The global decline in demand for commodity minerals and coal has negatively affected the US mining equipment manufacturing sector

Photo by Bloomberg

HARDSHIP AHEAD? Hillary Clinton leans toward the ‘liberal green ideology’, which will further spell hardship for the US coal industry

Photo by Reuters

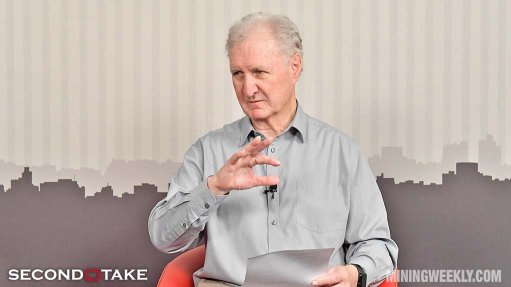

CHRISTOPHER ECCLESTONE Should Republican presidential nominee Donald Trump win, it would probably be a positive for the gold price

Photo by Christopher Ecclestone

The outcome of the November 2016 US Presidential election will not reverse the decline in the US mining industry’s value, as the beleaguered coal industry con- tinues to face market headwinds.

Rather, the results will determine the tra- jectory of environmental regulations and, therefore, raise or lower operating costs over the coming years, recent analysis from market analysis company BMI Research indicates.

According to the Fitch-owned research firm, regardless of the outcome of the November 2016 general election, the US mining industry value (MIV) will continue to decline through 2017, as elevated costs and structurally lower mineral prices weigh on growth.

The tightening of environmental regulations throughout the administration of President Barack Obama has accelerated this decline, both raising costs and edging coal – the domestic mining industry’s biggest contributor – out of the power mix.

The 2016 Presidential election will result in either the continuation and possible expansion of Obama’s environmental legacy, or an easing of and possible dismantling of emissions policies, dependent on the election of the Democratic or Republican nominee, respectively. The US and China formally ratified the COP 21 Paris climate agreement early in September at the G20 summit in China.

Election Jitters

While commentators view Obama’s two terms in the country’s highest office as being relatively uneventful, his legacy centres around lowering US emissions and driving the Clean Power Plan (CPP), aimed at cutting carbon pollution from existing power plants, thus dealing a severe blow to the domestic fossil-fuel industry.

According to principal and mining strategist at economic think-tank Hallgarten & Company Christopher Ecclestone, should Republican Presidential nominee Donald Trump win, it would probably be a positive for the gold price, as he is a harbinger of policy uncertainty, while Democrat nominee Hillary Clinton’s influence on the mining industry is largely unknown at this point, besides continuing the managed decline for coal, as she persists with Obama’s environmental policies, and a possible bump for steel under her robust infrastructure plan.

Ecclestone notes that Clinton leans toward the “liberal green ideology”, which will further spell hardship for the national coal industry.

“Neither Presidential candidate has spelled out in any detail how they would make good on their stated ‘support’ for the mining industry, so I believe it is too early to make specific predictions,” US National Mining Association (NMA) VP for external communications Luke Popovich tells Mining Weekly.

Generally speaking, Trump has been clearest in his stout defence of the coal industry and his intent to roll back some of the regulations put in place under the Obama administration.

Clinton has empathy for distressed coal communities, but is in opposition to the industry that supports them.

“Her chief campaign adviser, for example, has been steering this President’s antimining policies, especially against coal. And she candidly acknowledged that, as President, she would double down on some of those policies to put more coal companies out of business and miners out of their jobs. All of this can be dismissed as campaign rhetoric – or not,” Popovich cautions.

An Industry in Decline

New research by the Minerals Education Coalition (MEC) of the Society for Mining, Metallurgy and Exploration shows that, for 2016, each new-born US citizen will in their lifetime consume 15 000 lb per capita more in mined minerals, compared with the previous year’s statistics.

The MEC yearly calculates the amount of minerals and energy fuels that are consumed in the average lifetime of an American born in the current year. The MEC calculated the yearly mined resources used per capita in 2015 at 39 660 lb. With an average life expectancy of 78.8 years, the average American will need 3.13-million pounds of resources to provide the products and materials they will depend on in their lifetime.

For instance, every 2016 baby will consume 393 054 lb of coal, 72 893 gallons of petroleum, 7.08-million cubic feet of natural gas, 945 lb of copper and 1.59 oz of gold.

However, the US mining industry is in a state of decline, facing headwinds stemming from the strong greenback, stringent environmental regulations and lower commodities demand.

Coal drives the US MIV, accounting for about 45% of the total in 2015, according to BMI. While the US is a top global producer of several commodities, sectors such as copper and lead garner less scrutiny on the national political stage, which reduces their exposure to the election outcome.

BMI believes that US coal output will fall from 562-million tonnes in 2016 to 589-million tonnes by 2020, averaging a yearly decline of 6%.

“US coal miners will continue to rein in output and lay off workers to withstand the weak coal price environment over the next few quarters, and . . . the Powder River basin and Illinois basin are expected to remain relatively resilient over the Appalachian basin, owing to their respective lower operating costs,” BMI analysts state.

“What has been particularly disturbing about this administration is its seeming embrace of the ‘keep it in the ground’ movement against fossil fuels, a departure from where it started, which was a much more reasoned ‘all of the above’ energy policy that valued a diverse energy mix,” Popovich says.

“Will a Clinton Presidency continue on this path and ignore the ‘all of the above’ energy policy that has long guided government policy in this country? We may soon find out.”

The NMA believes that the unyielding Obama-led regulatory assault on coal – from rules on power plants that have forced a large portion of capacity out of the market to pending rules that will retire more and raise the costs of producing coal – has been and continues to be of greatest concern.

In fact, a new analysis by the King University School of Business and Economics puts the various factors in perspective. Its analysis shows that, until 2013, low natural gas prices did indeed depress coal consumption for electricity generation, but only to a point. Soon afterwards, US Environmental Protection Agency (EPA) regulations began to take their toll on coal-based power plants, surpassing gas as a factor in coal’s decline.

Regulations such as the EPA’s Mercury and Air Toxics Standards shuttered 62 000 MW of coal capacity, dropping coal consumption by an estimated 105-million tons, compared with what consumption would have been without the standards and similar regulations, according to the NMA.

Marginal Operations

Ecclestone agrees that the US coal industry is in major decline.

Domestic and international demand for coal has slackened; US export markets have deteriorated badly from major strength just four years ago. To compound matters, companies are struggling with debt from acquisitions and expansions before the market sank.

In the past several months, three of the largest coal mine operators, including Peabody Energy, Arch Coal and Alpha Natural Resources, have filed for Chapter 11 protection under the US Bankruptcy Code and it is highly likely that additional coal companies will seek bankruptcy protection.

Ecclestone believes that the real danger is that the coal producers have become marginal operations, losing out against natural gas in competing for generation. “With policy directives and investment into cheaper natural gas, coal is not expected to regain lost ground – once the coal generators close, they do not reopen,” he tells Mining Weekly.

According to him, the incumbent administration banked on sweeping pollution-limiting rules for coal-fired power plants as the main driver to cut future emissions — but the courts have put those rules on hold indefinitely, while emissions have fallen, owing to a significant increase in cleaner-burning natural gas, which Obama was slow to regulate.

“What lies ahead, should the CPP be enacted, is even more grim,” Popovich suggests.

The shale gas boom has unleashed a flood of low-cost natural gas into the power generation market since 2005, helping to drive down coal’s share from 51% to about 30% today. “Then add to these market forces a relentless regulatory assault on coal from the Obama administration – from rules on power plants that have forced a large portion of capacity out of the market to pending rules that will retire more and raise the costs of producing coal.”

Challenges Abound

Ecclestone says US gold producers operate at a disadvantage, owing to the strong domestic currency. By comparison, all three major gold currencies, comprising the Australian dollar, the Canadian dollar and the South African rand, are trading lower, proving to be significant tailwinds to costs for producers in those jurisdictions.

“The truth is, however, that there are many marginal gold mines at a price of around $1 200/oz and, even at $1 300, the gold price does not provide much respite for Nevada-based miners,” Ecclestone says.

US copper miners are also struggling under the strong dollar, eroding competitiveness on the global market. Ecclestone points out that many projects look good on paper, but need a better copper price to get off the ground.

Despite zinc having fared a lot better than its red base metal cousin, the price remains somewhat depressed from earlier forecasts, despite significant production cutbacks from major producers such as Glencore. Teck Resources’ Red Dog mine, in Alaska, remains the world’s single largest producer of the metal used to make corrosion-resistant alloys.

Ecclestone cautions that the US lithium market is currently circling bubble territory, noting, however, that, out of the bubble, should emerge a few real projects. “It’s ‘gopher pasture’ out in the desert and there exists no real record of success,” he points out.

The potential for a bubble lies in the project promoters who crawled out of the woodwork when it became apparent that a lithium supply gap was emerging, but who have little interest in pursuing resources or reserves.

The global decline in demand for commodity minerals and coal has also negatively affected the US mining equipment manufacturing sector and orders for new mining machines have consequently dwindled, causing widespread retrenchments and plant closures.

On the hard rock side of the industry, Popovich bemoans that NMA members are saddled with one of the least efficient and most time-consuming permit processes of the world’s mining regions. “It can take from seven to ten years here to get the necessary permit approvals for new mining projects. And possible increases in financial assurance requirements and related rules – if implemented – are also a great concern to this sector,” he says.

According to Ecclestone, while there are technological advancements that can help many miners, the industry is typically exceptionally slow on the uptake of these technologies. He points to bacterial oxidation and the industry’s slow response to this useful technology that can improve gold recoveries. “There is unfortunately no new technology to ride to the rescue of ailing miners,” he comments.

Fortunes Turn

However, Ecclestone expects financial markets to start opening up to project developers now that analysts agree that the commodity super-cycle has bottomed.

He notes that financing is opening up for several projects with strong metrics. Therefore, good projects out there (including coal) should start encountering an increasingly friendly market, as commodity prices start rising in general.

The first phase of recovery usually favours companies with projects in jurisdictions investors are familiar and comfortable with, such as Nevada, and North America and Europe in general, Ecclestone explains. After the “low-hanging fruit” have been financed and developed, investors turn their gaze to other lesser-known jurisdictions, such as in South America and Asia. Africa stands at the back of the line, owing to the deemed higher investment risks of these jurisdictions.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Projects

Latest Multimedia

Latest News

Showroom

ECG provides specialised electrical engineering services to the Mining, Utilities, Materials Handling and Industrial industries, with extensive and...

VISIT SHOWROOM

We supply customers with practical affordable solutions for their testing needs. Our products include benchtop, portable, in-line process control...

VISIT SHOWROOM

Press Office

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation