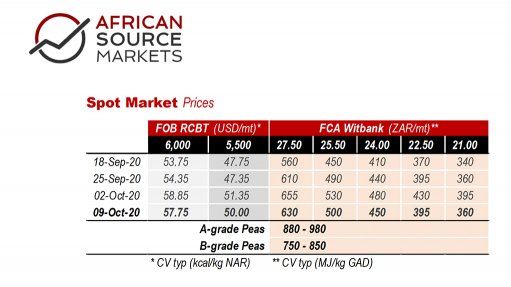

Photo by: African Source Markets

The Chinese ban on Australian imports has wrought confusion amongst traders, with many finding

innovative ways to get their cargoes sold.

Diplomatic relations between the countries soured ever since Australia’s ban on Huawei and blaming China for Covid-19. However, as coal supplies tighten ahead of Winter, China has apparently issued its northeastern Jilin province with import quotas for 5Mmt. One imagines there may be more of these “exceptions” to come, although as domestic mines in Inner Mongolia and Shanxi, China’s top two coal regions, raise production, the tightness in the northeast is expected to ease.

Vietnam is expected to significantly increase coal imports as domestic coal production becomes deeper and more expensive, and as local gas reserves deplete from 2022 onwards. We expect to see extended closures of up to 3 weeks at both Australian and SA mines for December, allowing for prices to recover, whilst also enabling extended maintenance on processing and logistics facilities.

Meanwhile, Ivan Glasenberg, the man who has defined the coal market, may have a point… Whilst other mining majors pursue buyers, who would probably extend coal mining, Glencore is instead running down its coal operations, without replacing them. Which approach is better for long term CO2 emissions? Climate activists will probably end up pressuring everyone.

The RB1 price has hit the top Bollinger and we are seeing a slight turn down in weekly momentum

(MACD) now. However, the signal line is pushing into positive territory which could help sustain pricing at these levels.

Momentum should recover upwards from here although one cannot imagine price shooting the lights

out, whilst it is pushing the top Bollinger higher.

However, unless we see some external bearish price pressures coming to bear (US elections, economic

uncertainty), there should be decent support for pricing at these levels.